I never realized until recently how the payment of the commission to an agent impacts the benefits and restrictions the client receives in a policy.

I had always been aware that a commission payment created the surrender period on a life or annuity policy. This is due to the fact that the insurance company needs a certain number of years to recoup the amount paid to the agent. That is why most life and annuity contracts contain a surrender schedule that lasts 7 – 10 years. It creates the long-term nature of these type of contracts.

I wasn’t aware, however, how the commission paid to the agent impacts the growth potential for a life or annuity contract.

I recently began a partnership with DPL Partners. They are an innovator of commission free insurance products.

This allows for the use of annuities that have no surrender and greater market participation. Let me give you an example…

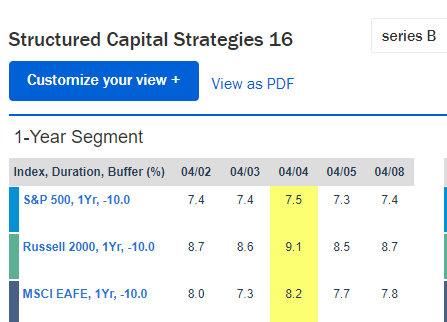

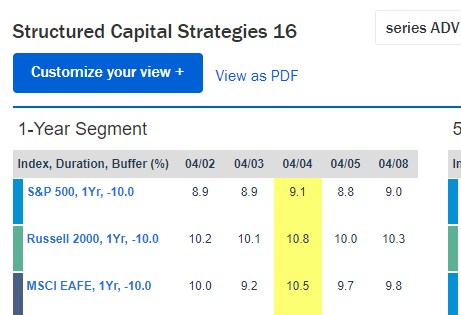

In the round of the Buffer Annuity, there is a commission based version (Series B) and a fee-based version (Series ADV).

The commission based version, Series B, has the following surrender schedule:

5% in the first year (declines each year afterward).

The fee-based series ADV contains no surrender or withdrawal charge.

The commission based version, Series B, has the following cap rates in their annual Buffer Annuity:

The fee-based series has the following cap rates on their annual Buffer Annuity:

Note that the fee-based annuity with no commission paid has a cap rate that is 2% per year higher.

What I’m finding is that this is the case across the board. DPL has negotiated and created products with top rated carriers that in many cases have

- No surrender fees with full liquidity

- Higher than industry average market participation

And now I’m looking at insurance options in a brand new light.

What made the trade-off of annuity products unpalatable for many was the long surrender schedules and the limited rates of participation and growth. With the new developments, both these issues have largely been eliminated making the implementation of various life and annuity product options much more attractive.

What’s your opinion on the use of annuities? What are the biggest turn offs for you? contact me and let me know.