The infographic found below is an extremely compelling one. I use it in my Maximizing Social Security course when talking about the value of delaying Social Security. What it communicates goes well beyond just Social Security planning and invites us to think about planning for longevity in all aspects of retirement.

It’s not uncommon to use life expectancy tables to consider longevity and the timing of Social Security break even points. Unfortunately, most life expectancy tables consider life expectancy from the standpoint of everyone, including babies and young children. In other words it includes the mortality of those in the early stages of life. The reality is, once you have reached the age of 65, the likelihood of higher longevity is significant.

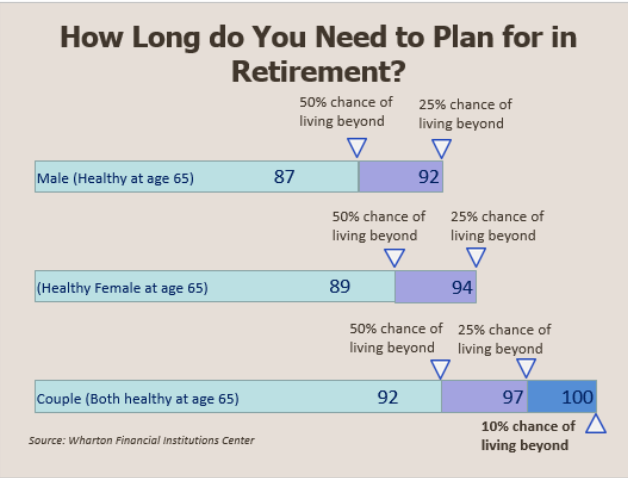

A healthy male at age 65 has a 1 in 2 chance of living to age 89 and a 1 in 4 chance of living beyond the age of 92.

A healthy female has a 1 in 2 chance of living to age 90 and a 1 in 4 of living beyond the age of 94.

A healthy couple has a 1 in 4 chance of one of them living beyond the age of 97, and a 1 in 10 chance that one of them will reach the age of 100.

It’s critical to build a retirement plan that can last for up to three decades of retirement. Many times it means maximizing Social Security for the primary income earner to make sure there are sources of guaranteed income that cannot be outlived and have the ability to grow over time inflation.

If you have any questions. Please feel free to contact me.